Tax-Advantaged Savings

Trump Account for Newborns: The Complete Guide to the $1,000 Baby Bonus and Form 4547

The Trump Account is a new tax-advantaged savings vehicle for children, created under the One Big Beautiful Bill Act signed on July 4, 2025. If you have a baby born in 2025, your child is eligible for a $1,000 government contribution. Here's everything you need to know.

Quick Summary

- $1,000 government contribution for babies born in 2025

- Child must be a U.S. citizen with valid SSN

- File Form 4547 to establish account and claim contribution

- Contributions to the account begin July 4, 2026

- Account converts to Traditional IRA at age 18

What is a Trump Account?

A Trump Account is a tax-advantaged individual retirement account for minors under age 18, established under Section 530A of the Internal Revenue Code by the One Big Beautiful Bill Act (Public Law 119-21). It's also referred to as a "530A account."

Think of it as a hybrid between a traditional IRA and a children's savings plan. The federal government seeds the account for eligible newborns, and families can make additional contributions. The funds grow tax-deferred until the child reaches adulthood.

Key Point: Trump Accounts offer flexibility beyond education savings. At age 18, the account converts to a Traditional IRA and can be used for education, home ownership, starting a business, or retirement.

$1,000 Pilot Program Eligibility

Children born in 2025 (through December 31, 2028) are eligible for the $1,000 government contribution if they meet all of the following requirements:

- U.S. citizen

- Valid Social Security Number (SSN)

- No income requirements (universal eligibility)

- Both parents must have SSNs (parent citizenship not required)

Key Point: There is no income limit or phase-out. Every eligible newborn qualifies for the full $1,000 contribution regardless of family income.

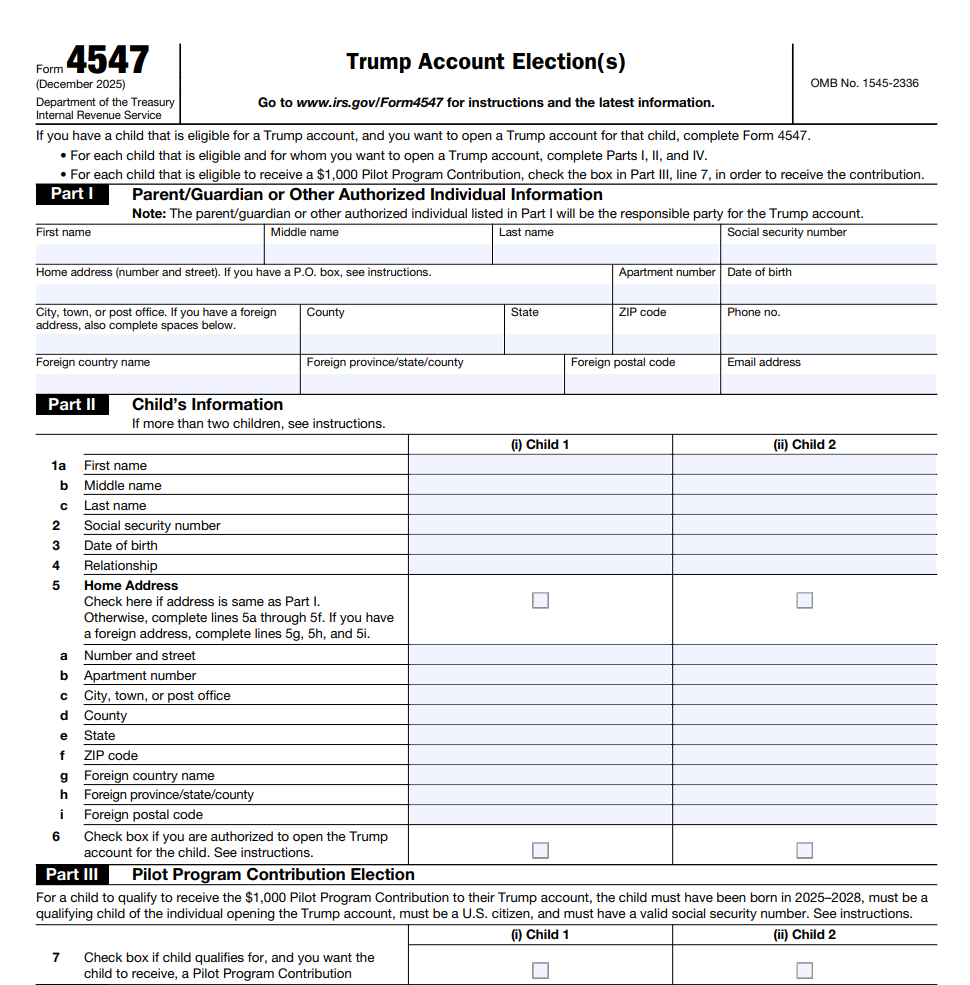

How to Open a Trump Account (Form 4547)

Form 4547 (Trump Account Election) is used to establish a Trump Account and elect the $1,000 pilot contribution. You must file this form to receive the government contribution.

Who Can File (Priority Order)

- Legal guardian

- Parent

- Adult sibling

- Grandparent

Filing Methods

- E-file with tax return: Attach to your 2025 tax return (due April 15, 2026) - Recommended

- IRS online portal: File standalone via IRS portal (available mid-2026)

- Paper form: Mail completed Form 4547

Form 4547 Checklist

- Part I: Filer information

- Part II: Child information (name must match SSN card exactly)

- Part III: Check box for $1,000 pilot contribution

- Part IV: Signature

If you have multiple eligible children, attach additional copies of Form 4547 for each child.

What If My Baby's SSN Hasn't Arrived by April 15?

This is a common situation for parents of late-year newborns. You have several options:

Option 1: File an Extension

File Form 4868 to extend your individual tax return to October 15, 2026. This automatically extends your Form 4547 deadline as well. Once you receive the SSN, complete Form 4547 and file with your extended return.

Option 2: File Tax Return Now, Form 4547 Later

You can file your 2025 tax return without Form 4547. Submit Form 4547 separately once the SSN arrives using the IRS online portal (available mid-2026) or by mailing the paper form.

Option 3: Wait for Online Portal

If you already filed your tax return, you can submit Form 4547 standalone through the IRS online portal launching mid-2026. The $1,000 contribution is not tied to your tax return filing date.

Important: Form 4547 requires a valid SSN before filing. The child's name and SSN must exactly match the Social Security card. Do not file with an ITIN or pending SSN application.

SSN Processing Times: Applications typically take 2-4 weeks when applied at the hospital, or 4-6 weeks by mail. Plan accordingly if your baby is born late in the year.

Contribution Rules

Trump Accounts allow contributions from multiple sources, each with different limits:

| Contributor Type | Annual Limit | Notes |

|---|---|---|

| Individuals (parents, family) | $5,000 per child | Includes all non-employer contributions |

| Employers | $2,500 per employee | Counts toward $5,000 limit; not taxable to employee |

| Federal Government | $1,000 (one-time) | Pilot program; does NOT count against $5,000 limit |

| Tax-exempt organizations | Unlimited | Charitable contributions allowed |

Key Rules

- First contribution date: July 4, 2026

- Contributions are NOT tax-deductible during the "growth period" (before age 18)

- Child does NOT need earned income (unlike regular IRAs)

- Employer contributions are excluded from employee's taxable income

Investment Options

Trump Account funds must be invested in qualified index funds meeting these requirements:

- Track a broad U.S. equity index (e.g., S&P 500)

- Expense ratio capped at 0.1%

- Primarily U.S. equities

- No leverage allowed

Not Allowed

- Individual stocks or direct stock selection

- Bonds or fixed income

- Cash or money market funds

- International-only funds or cryptocurrency

Qualified Withdrawals

Age-Based Access

| Age | Withdrawal Access |

|---|---|

| Under 18 | Generally no withdrawals (exceptions for disability) |

| 18-24 | Up to 50% for qualified purposes |

| 25+ | Full balance for qualified purposes |

Qualified Purposes

- Higher education expenses

- Job training / vocational education

- First-time home purchase (up to $10,000)

- Starting a small business

- Natural disaster expenses (up to $22,000)

- Birth or adoption of a child (up to $5,000)

Tax Treatment

| Withdrawal Type | Tax Rate |

|---|---|

| Qualified withdrawal | Long-term capital gains rate |

| Non-qualified withdrawal | Ordinary income + 10% penalty |

Timeline & Key Dates

| Date | Event |

|---|---|

| July 4, 2025 | One Big Beautiful Bill Act signed into law |

| Dec 2025 | Form 4547 released by IRS |

| April 15, 2026 | Form 4547 can be filed with 2025 tax return |

| Mid-2026 | IRS online portal for Form 4547 launches |

| July 4, 2026 | First contributions to Trump Accounts allowed |

| May 2026+ | Treasury sends account information to approved filers |

Let Us Handle Your Trump Account Filing

For clients with a newborn in 2025 who use Copper River Tax's individual tax return service, we will file Form 4547 free of charge. Our team ensures accurate filing so your baby receives the $1,000 government contribution.

Free Form 4547 filing is available exclusively for clients filing their 2025 individual tax return with Copper River Tax who have a baby born in 2025.

Frequently Asked Questions

Do I need to file Form 4547 to receive the $1,000?

Yes. The $1,000 pilot program contribution requires filing Form 4547 to establish the account and elect the contribution. Without filing, your child will not receive the government contribution.

Need more help? Contact usWhat if I miss the April 15, 2026 deadline?

Form 4547 can be filed at any time, not just with your tax return. However, filing with your 2025 return is the most efficient method. The IRS online portal will also be available starting mid-2026.

Need more help? Contact usHow is the Trump Account different from a 529 plan?

Trump Accounts are not limited to education expenses. They convert to Traditional IRAs at age 18 and can be used for education, home purchase, starting a business, or retirement. Additionally, the government provides a $1,000 seed for eligible newborns.

Need more help? Contact usCan both parents file Form 4547 for the same child?

No. Only one authorized individual can establish a Trump Account for each child, following the priority order: legal guardian, parent, adult sibling, grandparent.

Need more help? Contact usMy baby was born in late 2025 and I haven't received the SSN yet. What should I do?

You have options: (1) File an extension for your tax return, which also extends the Form 4547 deadline; (2) File your tax return now and submit Form 4547 separately once the SSN arrives; or (3) Use the IRS online portal launching mid-2026. The $1,000 contribution is not lost if you file Form 4547 after April 15.

Need more help? Contact usDisclaimer: The information provided in this article is for general informational purposes only and should not be considered tax, legal, or financial advice. Tax laws and regulations are subject to change, and individual circumstances may vary. Always consult a qualified tax professional for specific guidance regarding your tax situation. Copper River Tax is not responsible for any errors, omissions, or reliance on the information presented.